How are Options priced?

Introduction to Options

Options are derivative contracts which give the holder the right (but not the obligation) to buy (call option) or sell (put option) a security at a particular price before or at the expiration of the contract.

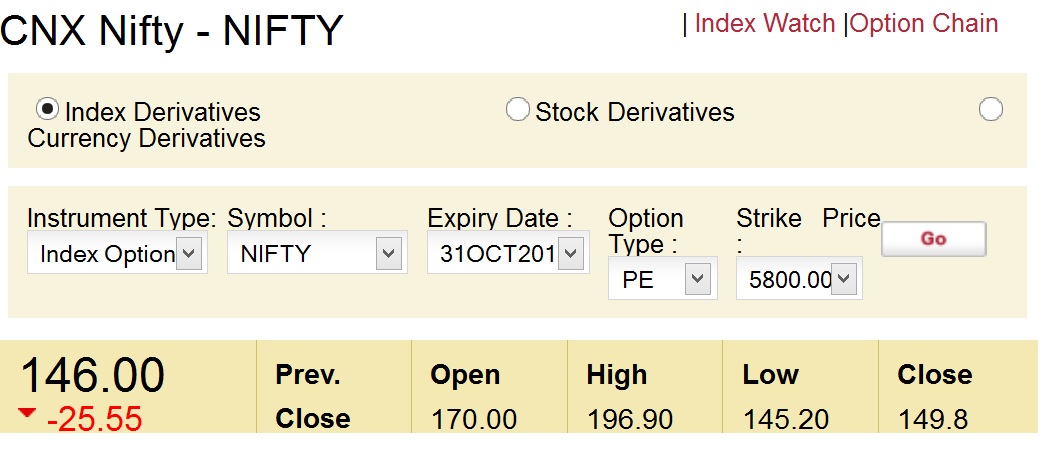

For example, a CNX Nifty put option (Benchmark Indian Stock Market Index) may look like

October 2013 PE 5800 having a lot size of 50, quotes at 146 on October 1st 2013.

This means that the contract expires by the last Thursday of October 2013 (31st). PE stands for Put European. European options can be exercised on expiry day only while American options can be exercised on any day.

Put options give the right to sell the underlying security (Nifty in this case) at 5800 which is called the strike price. It is the price at which you can sell the security.

So in our example, if Nifty is at 5400 on October 31st 2013, then the option holder can exercise the option which gives him the right to sell Nifty at 5800. But since its trading at 5400 on October 31st, he immediately pockets the difference of 400 points. (5800 which is the strike price – 5400 which is the current price on 31st Oct).

His profit would be equal to 254 (400 – 154) because he paid 146 to purchase this contract on October 1st.

Since the lot size is 50, both the profit and loss along with the cost need to be multiplied by 50 to arrive at the actual figures in Rupee terms. In this case our cost of buying the option would be Rs 7,300 (146*50) and our subsequent profit would be Rs 12,700 (254*50)

European options can be exercised only on expiry (31st October in this case) but can be sold anytime.

Options pricing explained

Options have two broad components in their price.

1) Intrinsic value

2) Extrinsic value

Intrinsic Value – If you were to exercise the option at this very instant, what would the value of the option be? That is the intrinsic value.

Extrinsic Value – Since you are not exercising your option now but you have “time until expiration”. There is uncertainty of what will happen till then.

To compensate for this uncertainty, option writers demand a premium over and above the intrinsic value. This premium depends on a lot of factors but mostly upon

1) Implied volatility (called Vega) – How volatile do the writers think the underlying is? A lot of the option price is determined by the implied volatility, especially in the case of options with volatile stocks as the underlying.

2) Time left till expiration (called Theta) – Its the time value of the option. The option decays by a small amount each day until expiry. It is very small initially (like 1/3rd of the time value in the first half) and accelerates as we near expiry (like 2/3rds in the second half).

3) Interest rates (called Rho) – As interest rates rise, the call value increases and the put value decreases.

That is because calls act as a proxy to buying shares. You can buy calls with a relatively small amount of money and keep the remaining money in a risk free bank deposit and earn more interest. This makes call buying more attractive increasing its price.

Buying puts are a proxy to selling shares. It is more attractive to sell actual shares than buying puts because you will get more money that way. That money which you get if you were to sell the shares can then be put in a risk free bank deposit and you can earn interest on it. That makes put buying less attractive thereby decreasing its price.

That is also the reason why deep in the money European put options with a lot of time left to expiration actually have a negative extrinsic value.

4) Dividends – As the price of the underlying falls when it gives dividends, the value of the call option falls as well. The value of the put option rises due to the fall in the underlying.

There are a couple of other things one need to know with respect to options

1) Delta – Probably one of the most important. Delta is basically how much the option moves when the underlying moves up by 1%. If the option price moves 0.5% if the underlying moves upwards by 1%, then its delta is 0.5. (Positive for call options). If it moves -0.5% (or moves down by 0.5%), then its delta is -0.5 which occurs for put options. (Remember – puts decrease in value as price of the underlying increases in value and that is why they have a negative delta).

Delta is highest for options that are in the money (have high intrinsic value) and lowest for those that are out of money (have no intrinsic value and are far away from the current spot price).

2) Gamma – It is the rate of change of delta. If delta is analogous to speed, then you can consider gamma to be like acceleration. Highest for at the money options, decreases as we go in the money or out of the money.

Short gamma is you lose money if the underlying moves. For example, if you write both call and put options.

Long gamma is you lose money if the underlying does not move. Example, if you buy both calls and put options.

These are some of the basics of options. In my next article I’ll delve a little deeper into each of the “Greeks” (Delta, Gamma, Vega, Theta, Rho) mentioned here and we will also look at some of the ways to make money trading options.

If you liked the article, please share it. If you have anything to say or ask, feel free to leave a comment in the comments section below.

Like our facebook page @ http://www.facebook.com/markets.sengukoi

Latest posts by Sengukoi (see all)

- MSCI Emerging Markets Index correlation with CNX Nifty - October 5, 2013

- How are options priced? - September 29, 2013

- Sensex chart since 1979 - September 24, 2013