MSCI Emerging Markets Index correlation with CNX Nifty

MSCI Emerging Markets Index

Its a stock market index which takes into account 817 stocks across 21 emerging market economies. It covers approximately 85% of all the emerging market economies based on the free-float method.

So, yeah. Its one of the broadest indices out there on the emerging markets.

It comes in many flavors as far as the currency denomination is concerned. Two of the popular ones are the dollar denominated MSCI EM index and local currency denominated MSCI Emerging markets index. Here local currency refers to the individual currencies of the constituent countries.

For my article, I’ll be taking the local currency denominated MSCI EM index.

CNX Nifty

Its the benchmark large cap index of the Indian stock market. It takes into account the largest 50 stocks and covers almost 70% of the free-float market cap of all the stocks listed on the exchange.

Its also important for an investor/trader as most mutual funds measure performance (alpha) with respect to it. There are also a lot of derivative contracts worth hundreds of millions of dollars linked to it. So, the index assumes a larger importance even though its not a broad based one.

The Correlation

The Indian component of the MSCI Emerging markets index is pretty small actually – at around 6.4% (August 2012) but still it seems to have a high correlation with the EM index.

To measure the historical correlation – I have taken the 300 day exponential moving average of the 20 period historical correlation of the MSCI Emerging Markets index with respect to the CNX Nifty. A correlation of over 0.7 is considered pretty good.

It turns out the historical correlation comes to around 0.71 which indicates a high degree of correlation.

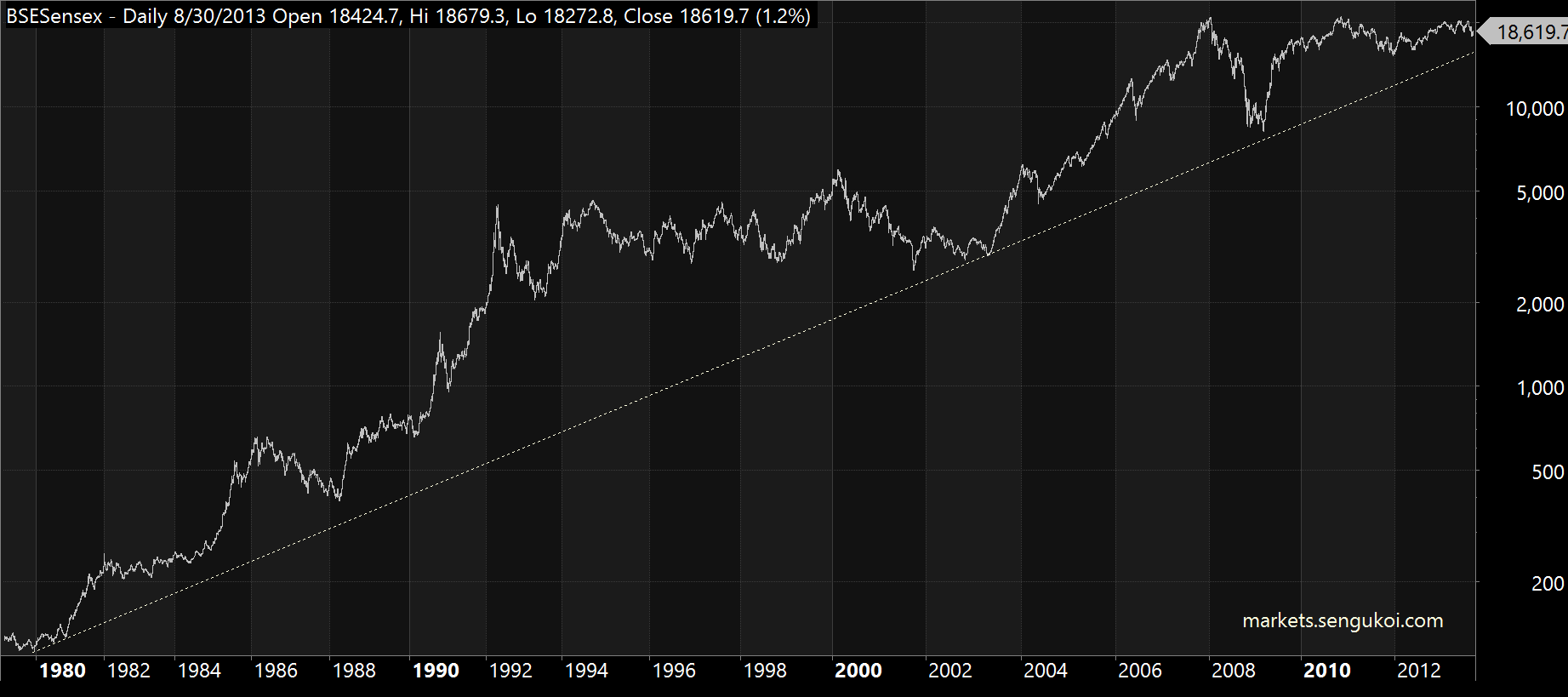

Technically as well, we can see a lot of patterns on both the charts to be pretty similar.

The image below is that of MSCI Emerging Markets Index (local currency)

The image above is that of CNX Nifty

Usefulness

Knowing the high correlation between these two indices can be pretty useful.

Important and sustainable trends usually seem to occur together on both the indices.

So, for example the break of an important support (such as the 5400-5500 support of the Nifty in August 2013) was not confirmed by a similar break in the MSCI EM index and as one can see, the market just retraced the move completely and now both the indices appear to be in synch again.

Conclusion

As the markets open up more and more to the outside world, they also seem to act in a more correlated fashion. What effects one part of the world no longer is confined to that region alone.

For now, most emerging markets appear to be in a synch with a few differences. There doesn’t seem to be as much correlation with the developed economies but as time passes, that gap might close up as well.

If you liked the article, please share it. If you have anything to say or ask, feel free to leave a comment in the comments section below.

Like our facebook page @ http://www.facebook.com/markets.sengukoi